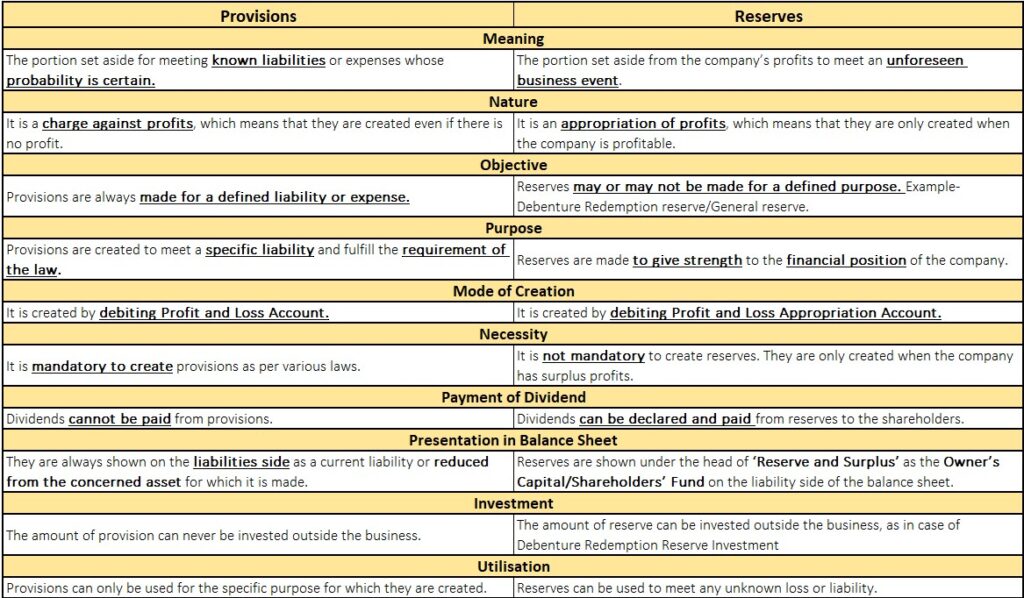

Difference Between Provision and Reserve

Provision

Provisions in accounting refer to amounts set aside by a company to cover potential future expenses or losses.

They are recognized as liabilities on the balance sheet, representing the company’s estimated obligation to meet certain expenses or liabilities that are likely to occur in the future.

Provisions are made when there is uncertainty about the timing or amount of an expense, but it is probable that the company will incur the expense.

They are typically based on reliable estimates and are made in accordance with accounting principles and guidelines.

Provisions can be categorized into different types based on their nature:

Provisions are adjusted over time as new information becomes available or as the estimates change. Any changes to provisions are reflected in the financial statements through appropriate adjustments.

Reserve

In accounting, reserves refer to amounts set aside from a company’s profits to meet future contingencies or to fulfill specific purposes.

Unlike provisions, which are created to cover potential losses or expenses, reserves are created to strengthen the financial position of the company or to allocate funds for specific purposes determined by management or legal requirements.

Here are some common types of reserves: