Hedge accounting is an accounting practice that allows companies to reduce the volatility in their financial statements caused by changes in the fair value of certain assets, liabilities, or transactions. It is primarily used to manage the accounting treatment of hedging activities undertaken to mitigate risks associated with fluctuations in interest rates, foreign exchange rates, commodity prices, or other market variables.

The main objective of hedge

accounting is to match the recognition of gains or losses on the hedged item

and the related hedging instrument, thereby providing a more accurate

representation of the company’s financial position and performance.

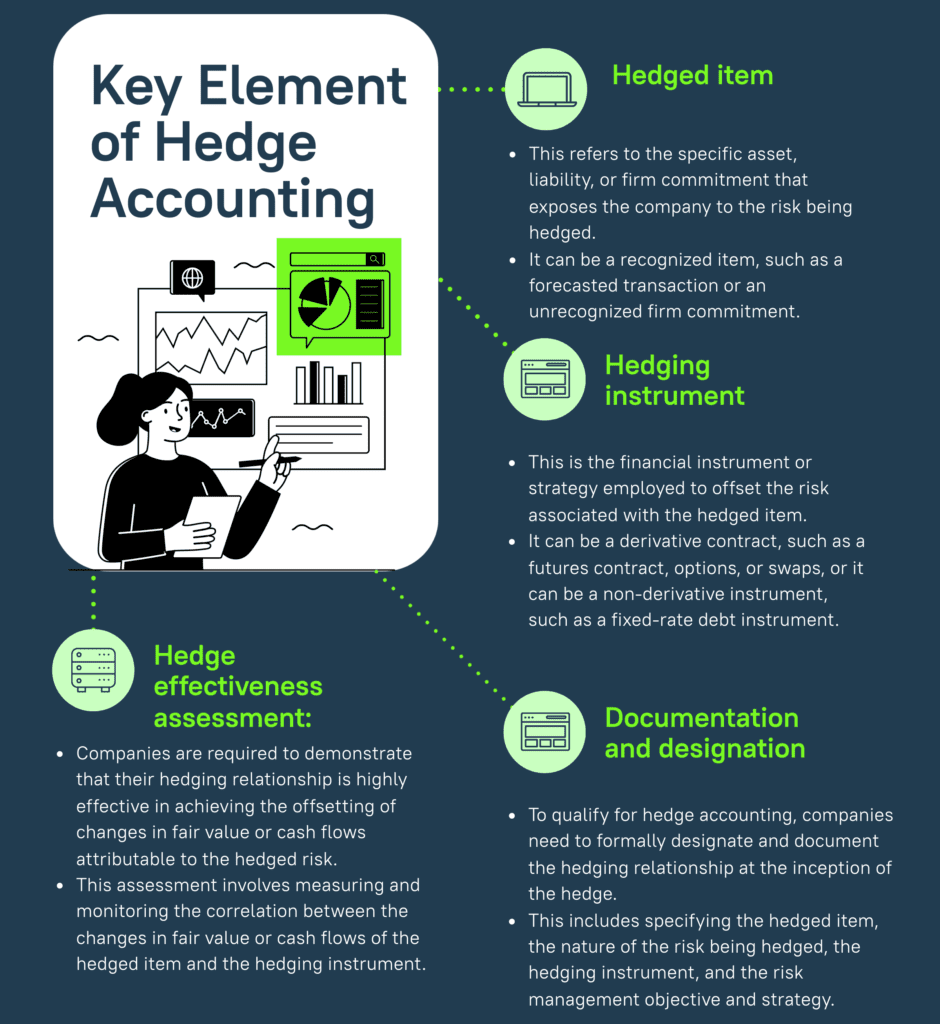

Key Element of Hedge Accounting

- 1. Hedged item: This refers to the specific asset, liability, or firm commitment that exposes the company to the risk being hedged. It can be a recognized item, such as a forecasted transaction or an unrecognized firm commitment.

- 2. Hedging instrument: This is the financial instrument or strategy employed to offset the risk associated with the hedged item. It can be a derivative contract, such as a futures contract, options, or swaps, or it can be a non-derivative instrument, such as a fixed-rate debt instrument.

- 3. Hedge effectiveness assessment: Companies are required to demonstrate that their hedging relationship is highly effective in achieving the offsetting of changes in fair value or cash flows attributable to the hedged risk. This assessment involves measuring and monitoring the correlation between the changes in fair value or cash flows of the hedged item and the hedging instrument.

- 4. Documentation and designation: To qualify for hedge accounting, companies need to formally designate and document the hedging relationship at the inception of the hedge. This includes specifying the hedged item, the nature of the risk being hedged, the hedging instrument, and the risk management objective and strategy.

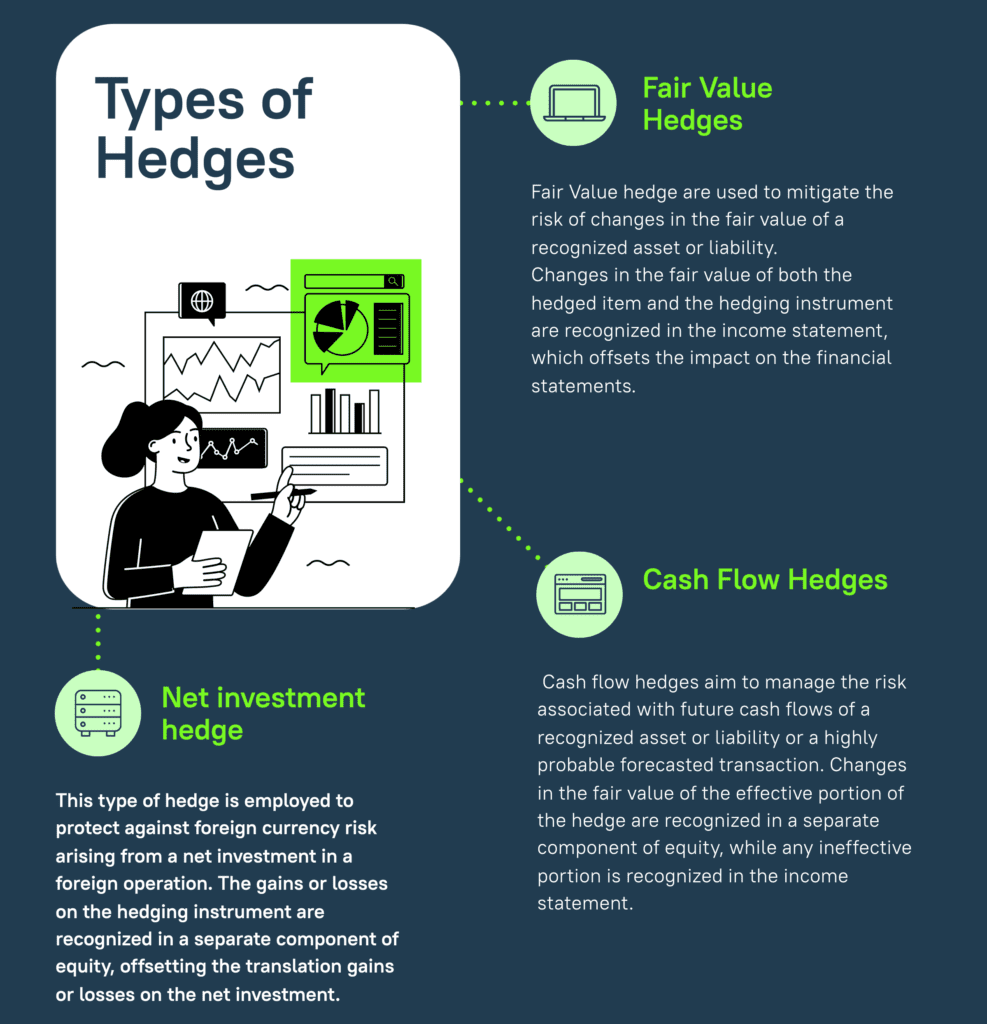

Types of Hedges

The accounting treatment for hedge accounting varies depending on the type of hedge being employed. There are primarily three types of hedges:

- 1. Fair value hedge: This type of hedge is used to mitigate the risk of changes in the fair value of a recognized asset or liability. Changes in the fair value of both the hedged item and the hedging instrument are recognized in the income statement, which offsets the impact on the financial statements.

- 2. Cash flow hedge: Cash flow hedges aim to manage the risk associated with future cash flows of a recognized asset or liability or a highly probable forecasted transaction. Changes in the fair value of the effective portion of the hedge are recognized in a separate component of equity, while any ineffective portion is recognized in the income statement.

- 3. Net investment hedge: This type of hedge is employed to protect against foreign currency risk arising from a net investment in a foreign operation. The gains or losses on the hedging instrument are recognized in a separate component of equity, offsetting the translation gains or losses on the net investment.

It’s important to note that hedge accounting is subject to specific rules and requirements outlined in accounting standards, such as International Financial Reporting Standards (IFRS) or Generally Accepted Accounting Principles (GAAP), depending on the jurisdiction and reporting framework used by the company.