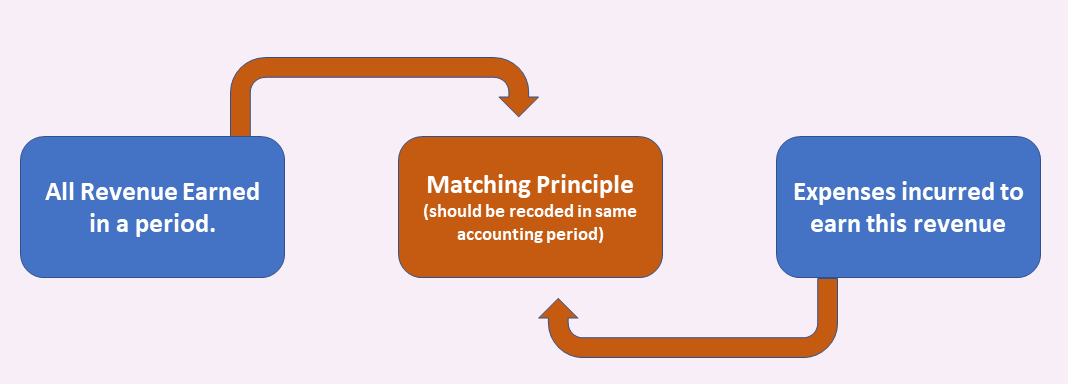

The Matching Concept, also known as the matching principle, is an accounting principle that guides the recognition of expenses in the same period as the related revenues they help generate.

It aims to accurately measure the profitability of a company by aligning the recognition of expenses with the revenues they contribute to earning.

Key points regarding the matching concept include:

1. Expense Recognition: The matching concept requires that expenses be recognized in the same accounting period as the revenues they help generate. This ensures that the costs associated with generating revenue are properly matched and allocated to the period in which the revenue is recognized.

2. Cause-and-Effect Relationship: The concept is based on the idea that there is a cause-and-effect relationship between revenues and the expenses incurred to generate those revenues. By recognizing expenses in the same period as the related revenues, it reflects the direct association between the two.

3. Accrual Accounting: The matching concept is closely tied to accrual accounting, where revenues and expenses are recorded when they are earned or incurred, regardless of the timing of cash flows. This allows for a more accurate representation of the financial performance of a company.

4. Period Costs: The matching concept applies to both direct costs (such as direct materials or direct labor) and indirect costs (such as rent, salaries, and utilities). Indirect costs are allocated or matched to the relevant periods based on a systematic and rational basis, such as the passage of time or activity levels.

5. Adjusting Entries: Adjusting entries are made at the end of an accounting period to ensure that revenues and expenses are properly matched. These entries may involve recognizing accrued expenses or prepaid expenses to align them with the related revenues.

The matching concept helps provide a more accurate picture of a company’s financial performance by associating expenses with the revenues they generate.

This principle is essential for generating reliable financial statements and facilitating better decision-making by stakeholders.

It allows for the assessment of a company’s profitability, helps identify trends and patterns in costs and revenues, and aids in the evaluation of the efficiency and effectiveness of business operations.