These golden rules serve as the foundation for recording transactions accurately and maintaining the integrity of financial statements. By following these rules, accountants ensure that the accounts reflect the financial reality of a business and facilitate accurate financial reporting and analysis.

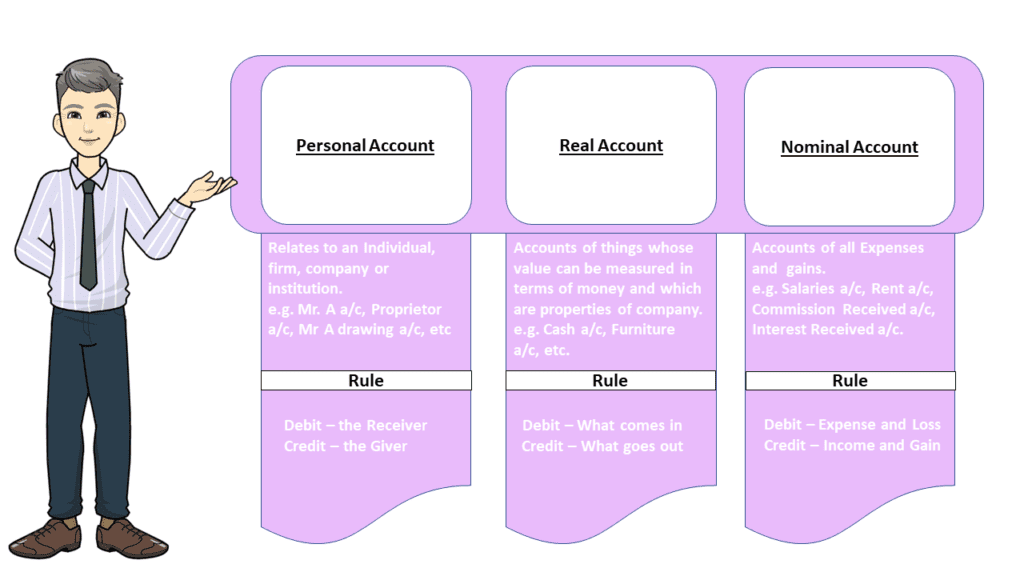

1. Personal Accounts Rule

Personal accounts refer to accounts that represent individuals, such as customers, suppliers, or the owner.

The rule for personal account is: “Debit the receiver, credit the giver.”

This rule applies when there is an inflow or outflow of goods, services, or money between individuals.

For example, if a customer pays for goods purchased on credit, you would debit the customer’s account (representing an increase in the customer’s balance) and credit the sales account (representing a decrease in accounts receivable).

2. Real Accounts Rule:

Real accounts pertain to tangible assets, liabilities, and owner’s equity.

The rule for real accounts is: “Debit what comes in, credit what goes out.”

This means that an increase in a real account is recorded as a debit, while a decrease is recorded as a credit.

For example, when cash is received, it is debited, and when cash is paid out, it is credited.

3. Nominal Accounts Rule:

Nominal accounts are related to revenues, expenses, gains, and losses.

The rule for nominal accounts is: “Debit all expenses and losses, credit all incomes and gains.”

This means that expenses and losses are recorded as debits, while incomes and gains are recorded as credits.

For instance, when an expense is incurred, it is debited, and when revenue is earned, it is credited.